05 February 2019

Bob Cunneen, Senior Economist and Portfolio Specialist

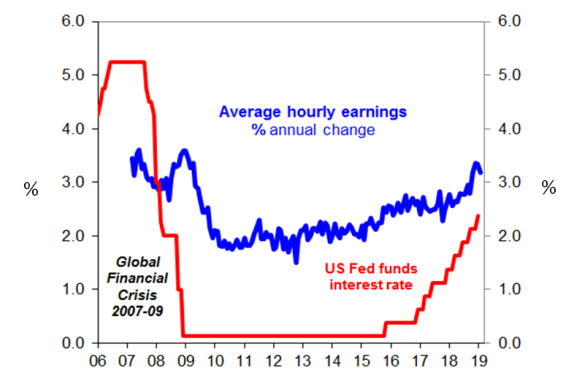

US interest rates (Fed funds interest rates) vs Wages (Average hourly earnings)

Source: Datastream.

The Federal Reserve (Fed) signalled at January’s policy meeting that it will be “patient” on future US interest rates settings given “global” conditions and “muted inflation pressures”. This comes after three years of raising the key Fed funds interest rates to the current range of 2.25% to 2.50% (red line). This can be favourably viewed as merely a temporary ‘pause’ in the Fed raising interest rates or, more ominously, as the end of the interest rate cycle as the US economy falters towards a recession.

The Fed is leaning towards the more positive assessment. Notably the Fed is still positive on the US economy given ‘solid’ economic activity and ‘strong’ jobs gains. January’s payrolls result also displayed that wages pressures are building as seen in the average hourly earnings measure posting annual growth at 3.2% (blue line). Essentially with the US unemployment rate falling to a multi-decade low of 4%, US employees now have more bargaining power to push for higher wages.

While the Fed can take some comfort that the current wage acceleration is mild by historical standards, the central bank cannot be complacent that US inflation pressures will remain ‘muted’. Current global worries such as President Trump’s Twitter tirades on trade, China’s slowdown, Brexit and Italy’s recession may temper price pressures for now. Yet with such a strong US jobs market and the potential for global surprises, the Fed’s pause on interest rates could end in a blink of an eye should US wages accelerate, commodity prices surge, or the US dollar dramatically falls.

Source : Nab assetmanagement February 2019

Important information

This communication is provided by MLC Investments Limited (ABN 30 002 641 661, AFSL 230705) (“MLC”), a member of the National Australia Bank Limited (ABN 12 004 044 937, AFSL 230686) group of companies (“NAB Group”), 105–153 Miller Street, North Sydney 2060. An investment with MLC does not represent a deposit or liability of, and is not guaranteed by, the NAB Group. The information in this communication may constitute general advice. It has been prepared without taking account of individual objectives, financial situation or needs and because of that you should, before acting on the advice, consider the appropriateness of the advice having regard to your personal objectives, financial situation and needs. MLC believes that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made as at the time of compilation. However, no warranty is made as to the accuracy or reliability of this information (which may change without notice). MLC relies on third parties to provide certain information and is not responsible for its accuracy, nor is MLC liable for any loss arising from a person relying on information provided by third parties. Past performance is not a reliable indicator of future performance. This information is directed to and prepared for Australian residents only. MLC may use the services of NAB Group companies where it makes good business sense to do so and will benefit customers. Amounts paid for these services are always negotiated on an arm’s length basis.